Who's winning the corporate vs. creator media economy tug-of-war? Sports fans.

These sports media brands have figured out fans want a buffet of content. So, let's eat

In early December, media veteran and Senior Advisor at the Boston Consulting Group Doug Shapiro published an article on his Substack, The Mediator. The article, ‘The Relentless, Inevitable March of the Creator Economy, ’ highlights an essential distinction between the two separate economies that make up the modern media space: the corporate economy and the creator economy.

The corporate economy involves legacy media institutions, both old and new. The New York Times, Netflix, Disney, Warner Brothers, etc. These entities manage risk and act as intermediaries between the hired creatives and their audiences, handling marketing, distribution, funding, promotion, packaging and more.

The creator economy — think independent creators who develop a direct relationship with their audiences via self-direction using platforms such as YouTube, Twitch, Substack, Instagram, TikTok, Spotify, etc. Shapiro describes this sector of the media economy as “all other media monetization.” Mr. Beast is probably the prime example of this phenomenon today, building his following on YouTube of over 342 million subscribers and achieving an annual revenue between $500-700 million per year.

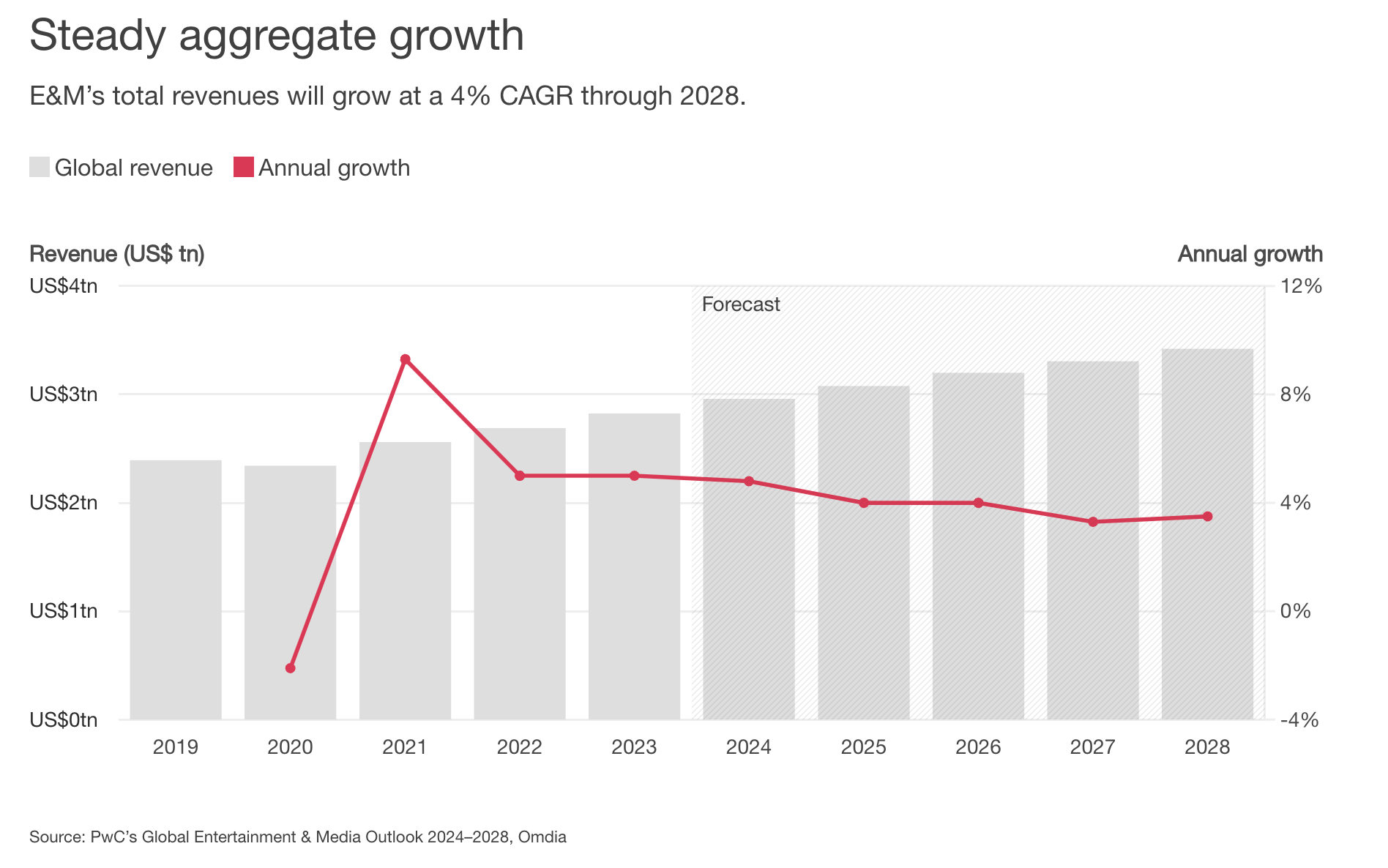

Since the invention of the Internet, the corporate economy has remained dominant in this tug-of-war battle. However, corporate levers are losing their lead as media consumption peaks. Not only is streaming leading the battle of where consumers are watching content, but in November 2024, YouTube was the leading streaming service, beating out Netflix by almost 3% — a trend that continues to grow.

This becomes even more prescient as growth in media consumption appeared to peak in 2021, most likely due to the pandemic’s effect on society. 2023 was the first year we saw consumption level out from the industry's headwinds in 2022, as seen below. With consumption habits maintaining a relatively steady pace, Shapiro argues that the corporate vs. creator battle is zero-sum, as data suggests consumers likely gravitate towards one form of media vs. another. We see this today as younger generations (young millennials, Gen Z and now Gen Alpha) consume more creator media vs. corporate media.

To say the least, this trend is not a bright one for the traditional media giants, as even new players like Netflix face headwinds from creator-centric platforms like YouTube, TikTok and Twitch. Well-known Media Universe Cartographer Evan Shapīro noticed the November 2024 trend in which creator media eclipsed corporate media, stating that this is just the beginning. He credits Doug Shapiro on helping him synthesize his predictions for the 2025 media landscape.1 He predicts that the creator sphere will take command of not only the revenue battle but the cultural battle as well this year:

The biggest ad platforms on earth are Creator-driven. The great irony of the Creator-sphere is that those who’ve traditionally had least power – artists & fans – now leverage the most powerful tech companies in human history to control the media they use. So many things in 2024 demonstrated this. Next year, the growing alliance between audiences and advertisers will tilt the cultural power dynamic even harder toward the Creator-sphere.

Despite this, corporate media institutions have and still hold several advantages. Large budgets, household brand names, and the ability to attract top-tier talent all culminate in a higher-quality product. However, they also face specific headwinds that affect the general consumer environment. These include the volume of creators and the ease of publishing. Additionally, with the acceptance and application of generative AI, the democratization of quality content will increase, blurring the quality distinction lines between corporate and creator media. They also face consumers’ rising distrust in central institutions and the demise of the monoculture. What does this mean for the corporate media environment? Well, Doug Shapiro poses that, at the very least, large media institutions need to accept this new reality as we enter a better-late-than-never domain.

For traditional media companies, the growth of creator media may be unsettling, but it’s time to move into the acceptance phase of the five stages of grief. There are only two choices: figure out how to participate in the creator economy or accept a perpetually shrinking business.

💡 Why sports is, once again, ahead of the curve

If there is one sector of media that has figured this out better and quicker than any other sector, it’s sports. Arguments have been made that the resurgence of cable news ratings, in the lead-up to and during Donald Trump’s first term in office (mid-to-late 2010s), stemmed from a strategy of emulating the likes of ESPN’s PTI, Around the Horn, and First Take.2 Below, I make the case that it’s happening again, but in the corporate-vs-creative dynamic, as old and new corporate sports media seem to have found a strategy that strikes a balance between corporate and creator media economies.

Is this true? If so, what is the sports media landscape doing? And how successful are sports media players in pulling it off? Is it the blueprint for the future?

📊 The “Dandex” breaks it down

The “Dandex” is a common theme throughout my articles. Simply put, it’s just a breakdown, but if you want to amuse me, it’s a simplified index categorized into different answers to the (why sports?) question presented above. This edition of the Dandex looks at four prominent trends that capture the evolution of the sports media ecosystem.

The blend of corporate sports media with creator sports media has been happening for some time. Still, sports media’s answer to the abovementioned problem comes in many shapes and sizes. Below, I break down some of the most influential and promising strategies we see across this industry today:

🤝 ESPN’s McAfee Acquisition

In May of 2023, the “World Wide Leader” signed Pat McAfee, former All-Pro punter for the Indianapolis Colts, to a five-year $85-million contract to broadcast and stream his show, The Pat McAfee Show, across ESPN’s airwaves and YouTube channel. While McAfee doesn’t necessarily meet the traditional mold of a “creator” laid out above, he is a prime example of how sports creators have leveraged their brands to partner with large media companies, ultimately culminating with the ESPN deal. After his playing career, Pat McAfee got his start in the media business at Barstool Sports. After creating the “Heartland” division, a new office for the company in Indianapolis, McAfee left the company after a lack of transparency in business operations practices.

After Barstool, McAfee incorporated his own small business (Pat McAfee Incorporated or PMI) before licensing his show out to different networks like DAZN, Westwood One, and SiriusXM and landing large sponsorships like FanDuel’s four-year $120 million agreement in 2021 to be the official oddsmakers of the show. This led to ESPN chairman Jimmy Pitaro’s relationship hitting a positive turning point as he and Disney CEO Bob Iger convinced McAfee to join the network, although retaining full creative control.

Drawing inspiration from ESPN’s collaboration with Peyton and Eli Manning through Omaha Productions, Pitaro has been instrumental in engaging talent who have made their mark on the football field and developed their distinct voices, whether through celebrity influence or prior media experience. This approach brings in authentic media figures with credible sports backgrounds and established audiences.

🧫 The Experiment that is Barstool Sports

You’ll notice a lot of cohabitation or cross-over of talent and strategies as we progress through this particular edition of the Dandex. No other place exemplifies this modern creator-and-corporate revolving door other than the successful sports-media-talent lab known as Barstool Sports.

Dave Portnoy, founder and President of Barstool Sports, began the Company in 2003 as a weekly print publication. After years of distributing a real-life newsletter full of gambling advertisements and fantasy sports projections in Boston, Portnoy took his venture online in 2007 following the explosion of the online blogosphere in the 2000s. Portnoy eventually set up shop in New York City in 2009.

Known as the “Bible of Bro Culture” and gaining in popularity, Barstool began to expand to different cities and college towns (under the brand BarstoolU), across the U.S. This expansion was preceded and engulfed with its fair share of controversies ranging from the sexualization of Tom Brady’s son to jokes about rape to underage drinking.

Despite this, Barstool continued to grow with 2016 standing out as a big year for the company:

Portnoy and Co. received investment from private equity firm The Chernin Group, which purchased a 51% majority stake at a valuation between $10 and $15 million.

Former AOL CMO Erika Nardini joined Barstool as its CEO.

Barstool bought Old Row Sports, another bro-centric sports blog, for an estimated $10 to $15 million.

Sports personalities Dan “Big Cat” Katz and PFT Commenter launched the comedic sports podcast Pardon My Take. The show is one of the top sports podcasts on Apple and Spotify.

The story of Barstool Sports was and continues to be a rollercoaster, but the primary takeaway is that the once-independent media company has established itself as one of the main players in the sports media ecosystem, rivaling corporate entities for talent development and acquisition. As mentioned earlier, Pat McAfee used Barstool as a launching pad but he’s not the only one. Alex Cooper, the host of the Call Her Daddy, had ties to Barstool Sports, beginning in 2018, before moving to SiriusXM. Call Her Daddy was the second most popular podcast on Spotify in 2021 and 2022, and recently had Vice President and 2024’s Democratic Presidential Nominee Kamala Harris on. NBA player Patrick Beverley and former NFL star Arian Foster have their own podcasts with the company. Comedian Grace O’Malley recently left the Barstool network to join Alex Cooper’s Unwell network after a controversy surrounding her pay. Sundae Conversation host Caleb Pressley also recently announced his departure from Barstool to start his company, Bill Joe Productions — which will partner with Tom Brady’s agency, Shadow Lion, and Underdog Fantasy.

Although Barstool still produces 71 podcasts and shows, it isn’t hard to see how the company has utilized creators and vice versa.

🎙️ Bill Simmons, his break from ESPN and the start of The Ringer

Like McAfee and Portnoy, sportswriter, podcaster and cultural critic Bill Simmons has a similar rise in the independent media sphere, although slightly reversed. The heart of Simmons’ career began at ESPN in 2001 as he earned a job offer from ESPN to write three guest columns as “The Boston Sports Guy.” In summary, Simmons became a key player in ESPN’s early digital strategy as the editor and chief of Grantland. This now-defunct sports and pop culture website started in 2011 and ended in 2015 after ESPN did not renew Simmons’ contract. Simmons’ conflicts with ESPN included public battles about creative freedom and censorship.

After a brief stint at HBO, Simmons began his own digital media outlet, The Ringer. The sports and pop-culture website and podcast network succeeded after Simmons recruited former Grantland and ESPN writers and hosts, such as Ryen Russilo, Mallory Rubin, Kirk Goldsberry and many more. Simmons also recruited Obama speechwriters Jon Favreau, Dan Pfeiffer, Jon Lovett, and Tom Veitor. These individuals went on to start their own media venture, Crooked Media.

In 2020, Spotify purchased The Ringer as part of its strategy to host podcasts on the primarily music-first streaming platform. Simmons claimed his venture was profitable just before the Spotify acquisition, as Forbes estimated the income of the network’s flagship product, The Bill Simmons Podcast, brought in $7 million annually. Simmons revealed that his show was the main reason he never took money from investors, telling hosts of the Smartless podcast that “ESPN didn’t care about podcasts.”

“ESPN didn’t care about podcasts at all, and we were convinced we can probably pay for everything with the podcast revenue,” Simmons told hosts Jason Bateman, Will Arnett, and Sean Hayes. “And I never ended up taking money from investors because we kind of felt like we could pay for everything through my podcast, which is what happened.”

Forbes called Spotify’s acquisition of The Ringer’s podcast network as “Podcasting’s First Big-Money Superstar.” In an interview with Bloomberg, Simmons got into the fulcrum of The Ringer’s content strategy — podcasts — arguing that the quality his network has found stems from authenticity rather than celebrity.

“Celebrity doesn’t matter with podcasts,” Simmons told Bloomberg’s Lucas Shaw. “What matters is, what’s your point of view? Are you consistent? Do you have a piece of turf you are trying to grab?

“We’ve always tried to be like the person you sit at the bar that’s fun to talk to knows shit. And you’re like, ‘Oh man! That was really fun to sit next to that person on the train and they knew this and this and this.’”

Simmons and The Ringer’s (and I would argue Barstool’s) success stems from that “guy at the bar” strategy. Casual, authentic conversations about low-risk topics, like sports are a theme that is emerging as the bow on top of the answer to the “why sports?” question posed above. McAfee, Barstool and The Ringer serve sports fans looking for these non-serious yet informative conversations. The next question is, well how can fans engage in such conversations? Well, let’s continue, shall we? ⤵️

📲 Bleacher Report brings players and fans closer together

Bleacher Report, similar to Barstool and Bill Simmons, began during the explosion of the blogosphere in the mid-aughts. “B/R” was a key player and rather effective at executing that strategy, but the evolution of the digital media company has set it apart from other sports websites founded in the 2000s.

The sports and sports-culture-focused company has expanded its presence across the internet over the past 15 years, focusing strongly on the younger millennial, Gen Z and Gen Alpha demographics. Let’s break down some of the stats3:

B/R is one of the most recognized sports media brands on social media:

19.4 million followers on Twitter/X

22.4 million followers on Instagram

4.43 million subscribers on YouTube

9.3 million followers on TikTok

B/R acquired sports UGC-powered social media behemoth House of Highlights in 2016, pairing the two social media titans.

In partnership with House of Highlights, the two have successfully cultivated the Creator League, a sports league for creators. HoH pairs up creators across the content spectrum and has them play basketball, dodgeball, etc., with or against each other, streaming the events live across social platforms.

The company produces its owned and operated shows, video podcasts (known as vodcasts), animated shows and player-led live and post-game coverage.

“We thought strategically about investing in video and podcasts,” general manager of Bleacher Report Bennett Spector told the Hollywood Report in 2023. “We always look at consumption trends, and how sports fans and consumers are engaging with content, and Bleacher Report being really a sports platform for the next generation. A lot of how younger people and younger sports fans are consuming is around live and interactive video.”

In May 2024, B/R announced Micah Parsons, the star defensive end for the Dallas Cowboys, as the President of their pro football brand, B/R Gridiron. In addition, his show The Edge continues to air live on the B/R app.

Bleacher Report has made similar but less extensive deals with other athletes, such as Deebo Samuel, Trae Young, Travis Hunter, and Mookie Betts. These athletes host their shows while continuing their day jobs — playing professional or collegiate sports.

The animation team has tapped into different intersections of culture and sport. Award-winner Game of Zones strategically blended storylines from a particular NBA season with those from the HBO hit Game of Thrones.4 Other animated shows include an anime-inspired NBA show, Hero Ball, and an NFL show set in a fictional town where all players, coaches, and owners live and work together, Gridiron Heights.

Fan and community engagement is also key to B/R’s strategy with a proprietary mobile app that encourages fan discussion as part of the content experience.

In a format similar to a social media site, users can comment on and react to various content types, such as articles, videos, photos, or animations. They can also send messages and follow one another.

B/R’s creator program allows screened users who are accepted into the “creator program” to go live and broadcast video directly in the app as part of specific fan communities. Typically, these users react to news, such as a game result or a coach firing.

All of this growth and strategy formation happened after B/R was acquired by Turner Sports in 2012. Now, the digital media platform is one of the core brands under the TNT Sports (and Warner Bros. Discovery) umbrella, which sets it apart as a critical case study in this corporate-vs.-creator environment.

The platform-ization of sports media brands

If the creator takeover of corporate media is inevitable, then the blend of these two media economies is worth paying attention to. The examples above, as well as the emergence of other platforms like FanDuel Sports Network, DraftKings Network, Playmaker Podcast Network and others that have signed current and former athletes (and even rebranded regional sports networks, in regards to FanDuel) to podcast shows, represent the smörgåsbord sports fans find every time they open their smartphones or laptops.

It’s becoming clear that the likes of TNT Sports and ESPN’s participation in the creator economy looks like an evolution from brand to platform — offering their production quality, large staffs and distribution networks as a product, like how YouTube offers their platform to any creator with a video camera.

As these large networks, including Barstool Sports and The Ringer (especially in regards to talent recruitment and development), start to enter the creator economy, entrenched legacy advantages will still ring true while creators bring authenticity and a built-in audience. Suddenly, this tension between creators and corporations looks more like a family cookout than a tug-of-war battle, and every sports fan is invited to chow down. Whether it’s fresh-off-the-grill authenticity or an independent craft beer with the distribution networks of a brand name, the sports media world is putting together one hell of a content buffet.

Quick shout out to Doug here — he is absolutely brilliant on this topic. I can’t recommend his Substack enough, even if you are one-tenth of the media business nerd I am.

Back in college, when I was an overwrought 20-year-old, I wrote an essay highlighting Trump’s run-up to the 2016 election. Part of the essay, which is now somewhere in the archives of the internet (as it was written for a now-defunct online magazine), highlights a thesis of comedian Bo Burnham that political media emulates ESPN debate shows, where the characters arguing about sports/politics are more critical to the argument rather than the actual argument they are making.

One note tying all of Bleacher Report’s content together is how it is packaged for different platforms. For example, the packaging for YouTube is different from that for Instagram, the B/R app, etc. This allows longer-form content to live and breathe on different platforms in different forms as part of a larger content strategy.

Bleacher Report and HBO are subsidiaries of the same parent company, Warner Bros. Discover.